Inflation, deflation, stagflation?

In early 2021, the Financial Times interviewed Equity Edge for an article about his career as co-founder and CEO of global investment firm Cambridge Associates and co-developer, along with clients and colleagues, of the celebrated university investment model. In that article, he warned that: “All investors need a bigger inflation hedge.”

Shortly after the interview was published, reported inflation in the U.S. climbed. In fact, between the time of the interview in March 2021 to May 2022, inflation skyrocketed 6%. What did Hunter have in mind when he wrote about “a bigger inflation hedge?” What is an inflation hedge? How and why should an investor hold one?

The term inflation hedge refers to a part of a portfolio specifically designed to earn a positive return when inflation is rising, a time when other returns would normally be expected to fall.

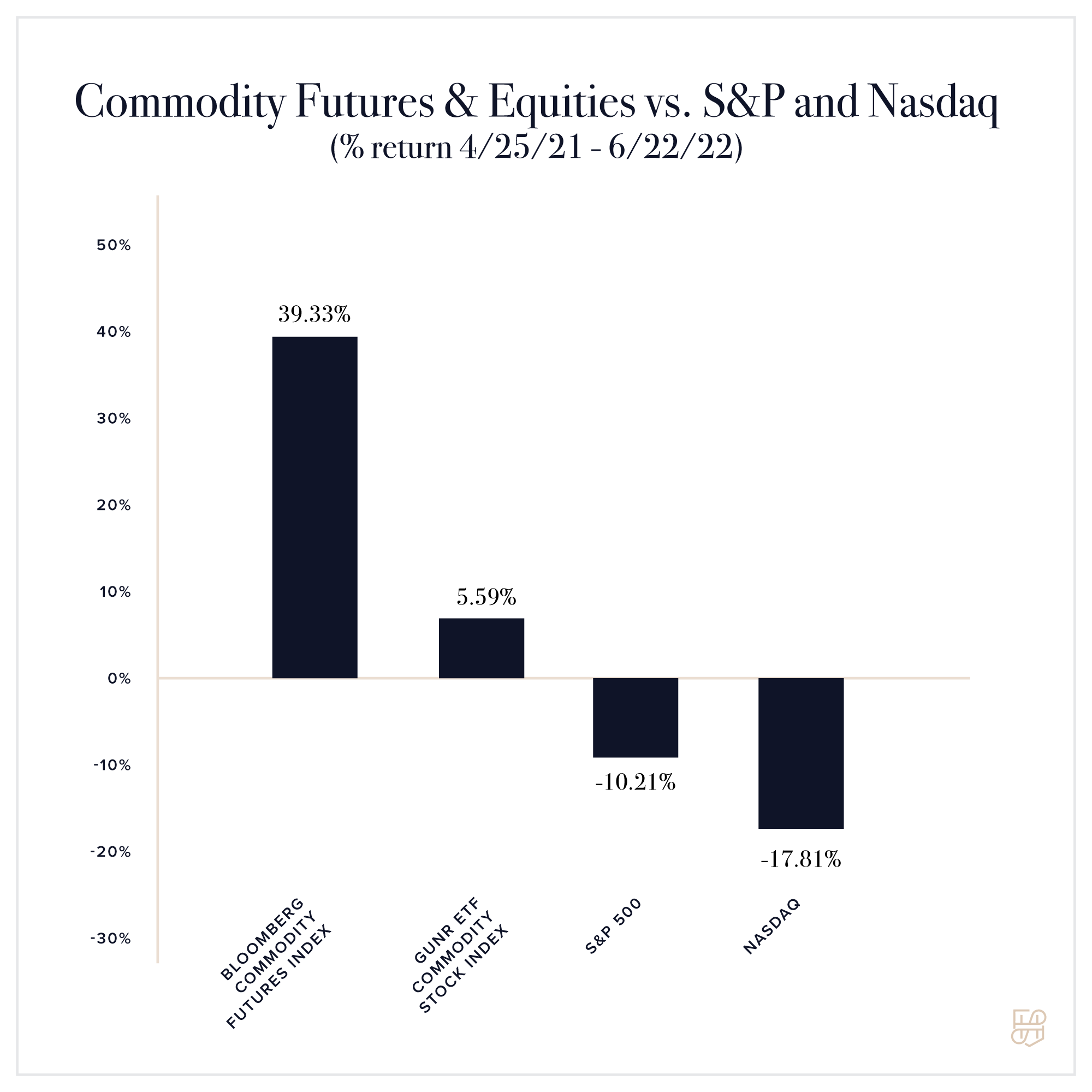

For example, here is the return of commodity stocks, often included in an inflation hedge portfolio, since the time of Hunter’s interview. Compare it to the return of the NASDAQ index, full of high-tech stocks, or the S&P 500.

Hunter first developed the idea of an inflation hedge portfolio decades ago. It is complemented by a deflation hedge portfolio which is intended to protect against recession, depression, or a financial crisis. Over the years, Hunter has increased or decreased his hedge portfolios depending on his outlook. In the spring of 2021, he was saying that it was time to increase the inflation hedge. These hedge portfolios are a way of controlling risk. When adequate hedges are in place, the rest of the portfolio can be invested with a greater degree of safety.

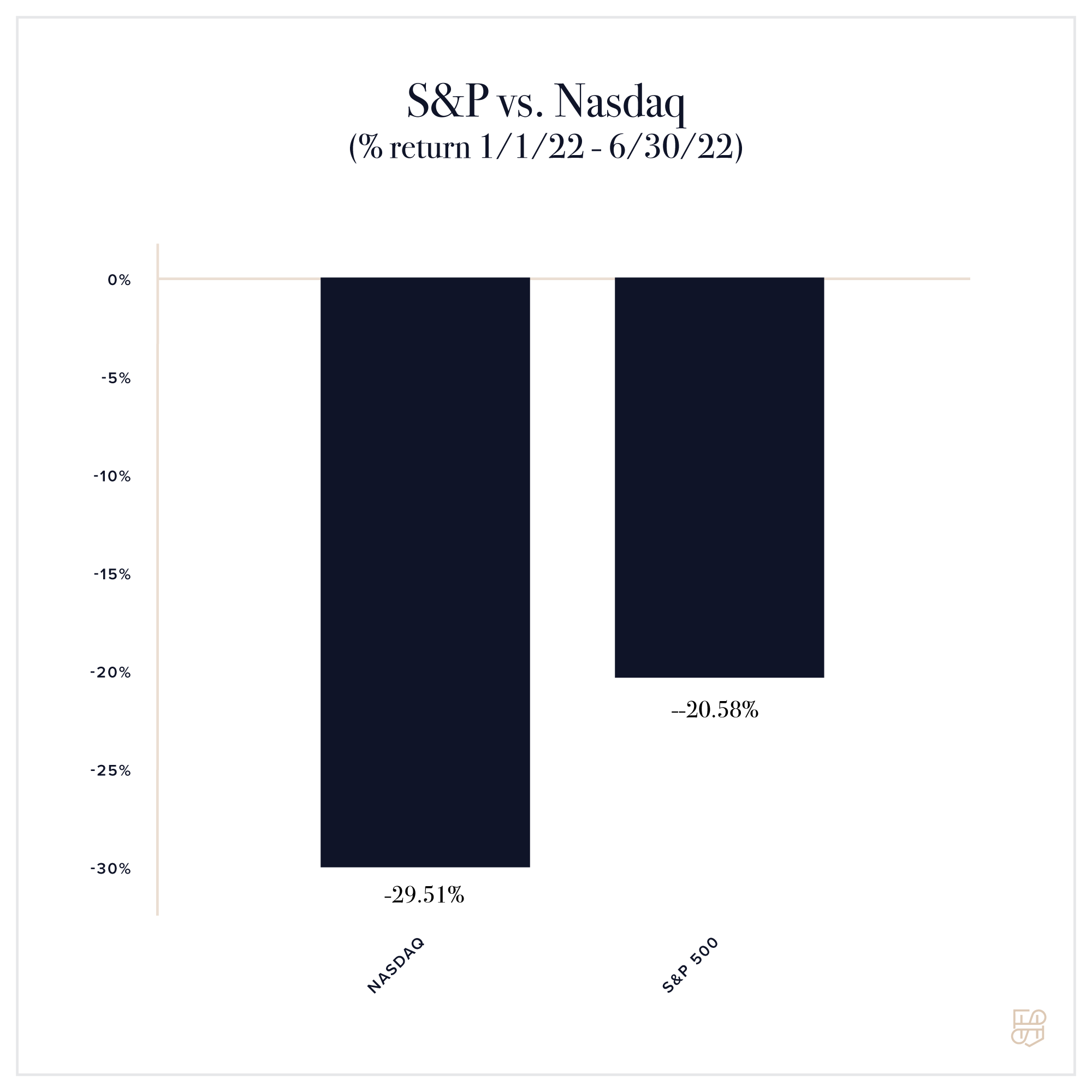

Sometimes investors need both an inflation and a deflation hedge portfolio at the same time. This is particularly true under conditions of stagflation and may be exacerbated by a runaway bull market, which has elevated stock prices to very high levels. On January 2022, Hunter wrote an article entitled “Bubble Trouble.” At the time there were 138 companies trading on the U.S. stock exchanges with a market capitalization of $10 billion (big companies) that had a price to sales ratio greater than 10. This meant that investors were paying ten times sales per share, an extraordinarily high price indicative of an investment bubble. Here is the return of the NASDAQ index and S&P 500 since then: